Formsy

Formsy

Partnership Firm Registration Online in India

Register your partnership firm legally under the Indian Partnership Act, 1932 and start business operations with confidence.

- Expert Partnership Deed Preparation & Drafting

- PAN & TAN Application Assistance

- Certified Legal & Compliance Support

- Quick & Efficient Registration Process

Enter your details to receive a full quote and consultation

What is a Partnership Firm Registration?

A partnership firm is one of the most important forms of a business organization. It is a popular form of business structure in India. A minimum of two persons are required to establish a partnership firm. A partnership firm is where two or more persons come together to establish a business and divide its profits amongst themselves in the agreed ratio. The partnership business includes any kind of trade, occupation and profession.

The Indian Partnership Act, 1932 governs and regulates partnership firms in India. The persons who come together to form the partnership firm are known as partners. The partnership firm is constituted under a contract between the partners. The contract between the partners is known as a partnership deed which regulates the relationship among the partners and also between the partners and the partnership firm.

Key Features and Purpose of a Partnership Firm

A partnership brings together multiple people to run a business and share its rewards and risks.

- Minimum Two Partners: At least 2 persons required; maximum 50 partners allowed under Indian Partnership Act, 1932.

- Mutual Agency & Shared Management: Each partner acts as an agent with authority to make binding business decisions and enter contracts.

- Profit & Loss Sharing Ratio: Partners share profits and losses as per partnership deed; equal distribution if no ratio specified.

- Unlimited Personal Liability: Partners bear unlimited liability for a firm's debts using personal assets if business funds are insufficient.

- No Separate Legal Entity: A firm has no distinct legal identity separate from partners; cannot sue or hold property independently.

- Voluntary Contractual Agreement: Partnership formed through mutual consent via partnership deed; dissolution by agreement, death, or retirement.

- Legal Recognition & Contract Enforcement: Registration provides legal standing to file lawsuits, enforce contracts, and protect partnership rights in disputes.

- Enhanced Banking Access & Credit Facilities: Banks and financial institutions prefer registered firms for current accounts, business loans, and credit approvals.

- Tax Deductions & Pass-Through Taxation: Access to business expense deductions, simpler tax filing procedures, and profits taxed at individual partner level.

- Increased Business Credibility & Trust: Customers, suppliers, and government agencies prefer working with registered firms; enhances market reputation. Protecting the firm’s name through trademark can further improve market trust.

- Property Ownership Rights: Registered firms can buy, sell, lease, and own property directly in the firm's name.

- Legal Dispute Resolution Framework: Clear legal mechanisms for resolving conflicts with partners, clients, suppliers, or third parties through courts.

Laws Governing Partnership Firm Registration in India

Partnership firm registration in India is mainly governed by the following laws and regulations:

- Indian Partnership Act, 1932: Core legislation governing partnership formation, partner rights and duties, firm operations, profit-sharing, and dissolution procedures in India.

- Income Tax Act, 1961: Governs taxation of partnership firms, including income computation, return filing, deductions, and tax payment obligations.

- Goods and Services Tax (GST) Laws: Mandatory GST registration for firms with turnover exceeding ₹40 lakhs (goods) or ₹20 lakhs (services); covers GST compliance and filing requirements.

- Indian Contract Act, 1872: Applies to partnership agreements ensuring contractual validity, enforceability, and legal obligations between partners.

Regulatory Authorities

- Registrar of Firms (ROF): State-level authority processing partnership registration applications, maintaining records, and issuing certificates under Indian Partnership Act.

- Income Tax Department: Issues PAN and TAN for firms; oversees income tax compliance, return filing, and tax assessments.

- GST Department (CBIC): Manages GST registration through GST portal, monitors compliance, and enforces GST laws for partnership firms.

- Local Municipal Authorities: Administer Shops and Establishment Act registration, issue trade licenses, and ensure municipal compliance.

Types of Partnership Firms Eligible for Registration

- General Partnership (GP): All partners share equal management responsibility and bear unlimited personal liability for business debts.

- Limited Partnership (LP): Includes at least one general partner (unlimited liability, active management) and limited partners (liability restricted to capital contribution, no management role).

- Limited Liability Partnership (LLP): Hybrid structure with limited liability protection for all partners; separate legal entity governed by LLP Act, 2008.

- Partnership at Will: No fixed duration; continues indefinitely until dissolved by partner notice or mutual agreement.

- Particular Partnership (Fixed-Term): Formed for a specific project or predetermined time period; automatically dissolves upon completion.

- Registered Partnership: Formally registered with Registrar of Firms; provides legal standing to enforce contracts and file lawsuits.

- Unregistered Partnership: Operates without ROF registration; lacks legal standing to sue or enforce contracts in courts.

Eligibility Criteria for Partnership Firm Registration

To register a partnership firm in India, you must meet the following conditions:

- Minimum Two Partners Required: At least 2 individuals must form the partnership; maximum 50 partners allowed under law.

- Written Partnership Deed Mandatory: Draft and sign partnership deed on stamp paper defining profit-sharing, roles, responsibilities, and capital contributions.

- Lawful Business Objective: Business must have legal purpose, operate for profit-making, and comply with Indian laws.

- Only Natural Persons as Partners: Only individuals (natural persons) can become partners; companies or legal entities excluded from traditional partnership firms.

- Age Requirement - 18 Years Minimum: All partners must be at least 18 years old and legally capable of entering valid contracts.

- Valid Identity and Address Proof: Each partner must provide government-issued ID (PAN, Aadhaar, passport, voter ID) and current address documentation.

- Mentally Sound and Solvent: Partners must be mentally competent and not declared insolvent or legally disqualified from managing business.

- Mutual Consent of All Partners: All partners must voluntarily agree to partnership formation and terms.

- Indian Resident Partner Requirement: At least one partner must be an Indian resident.

- Unique Firm Name: Firm name must not be identical or similar to existing companies, LLPs, trademarks, or registered partnerships.

- Registered Office in State: Partnership firm must have a registered office address in the state where registration is sought.

Documents Required for Partnership Firm Registration

To streamline the partnership firm registration process, make sure you have the following essential documents ready:

Essential Documents

- Partnership Deed: Comprehensive partnership agreement on stamp paper defining terms, roles, profit-sharing, capital contribution, and partner responsibilities.

- PAN Cards of All Partners: Self-attested copies of Permanent Account Number (PAN) cards for each partner.

- Residential Address Proof: Valid address proof for each partner: Aadhaar card, passport, voter ID, driving license, or utility bills.

- Business Address Proof: Documents verifying registered office address (property tax receipt, electricity bill, or rent agreement). Where acceptable, a virtual office address may also support registered office documentation.

- Passport-Size Photographs: Recent passport-size photographs of all partners (2-3 copies each).

Additional Documents (If Applicable)

- Rent/Lease Agreement: Copy of valid rent or lease agreement if operating from rented premises.

- No Objection Certificate (NOC): NOC from property owner granting permission to use premises for business operations.

- Utility Bills: Latest electricity, water, or gas bill for business premises as address verification.

- Bank Statements: Recent bank statements (3-6 months) of all partners as proof of financial identity.

- Identity Proof of Partners: Aadhaar card, voter ID, passport, or driving license for identity verification.

Partnership Deed Mandatory Contents

- Full legal names and current residential addresses of all partners

- Nature, scope, and objectives of the business

- Capital contribution amount by each partner

- Profit and loss sharing ratio agreed among partners

- Roles, rights, duties, and decision-making authority of each partner

- Duration of partnership (fixed-term or at-will)

- Admission, retirement, and expulsion procedures for partners

- Dispute resolution and arbitration mechanisms

- Dissolution and asset distribution terms

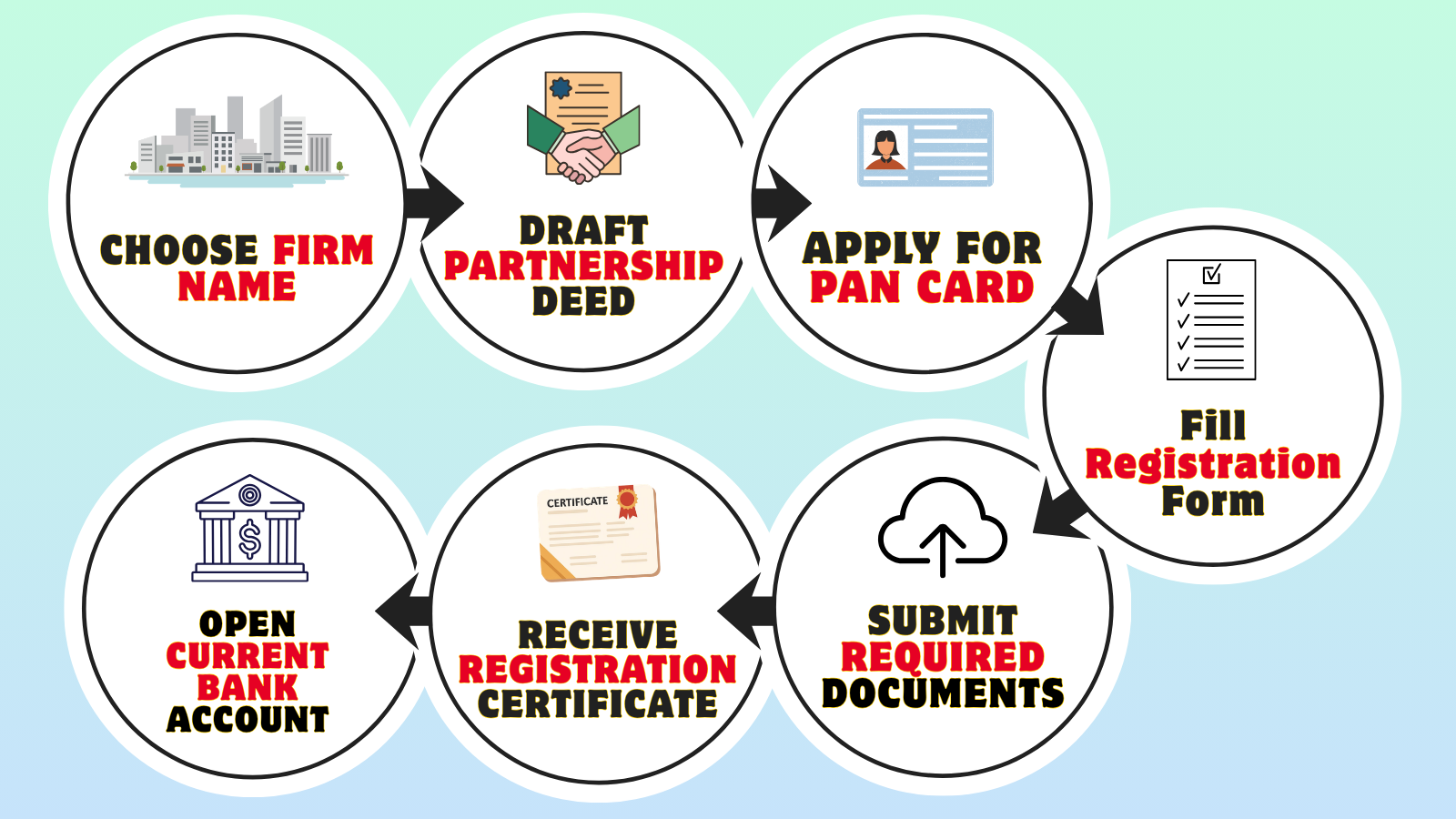

Step-by-Step Guide on How to Register a Partnership Firm

Follow this step-by-step procedure to complete the registration of a partnership firm efficiently:

-

Choose a Name for Your Partnership Firm

Pick a unique and relevant name that complies with state regulations. Make sure your chosen name reflects your business activities, doesn’t match existing registered firms in your state, avoids misleading or restricted words, and doesn’t confuse the public or resemble a government body. Check name availability on your state’s Registrar of Firms portal. Since firm names are registered at the state level, similar names may exist in different states. It should also avoid conflicts with existing trademarks. Prepare two or three alternative names in case your first choice is unavailable or rejected.

-

Draft the Partnership Deed

Prepare a detailed Partnership Deed that defines the structure and functioning of your firm. It should include names and addresses, business scope, capital contributions, profit/loss ratio, duties, and rules for partner admission/exit. Sign the deed on non-judicial stamp paper of appropriate value (as per your state’s rules). All partners must sign the document in the presence of witnesses. Notarize the deed to enhance its legal validity.

-

Obtain a PAN Card for the Firm

After you and your partners execute the partnership deed, you must apply for a Permanent Account Number (PAN) card in the partnership firm's name. The firm mandatorily needs this for tax purposes and to open a bank account. You can complete this application online through the NSDL or UTIITSL websites. It is also essential for income tax return and broader tax compliance.

-

Fill Out the Application for Registration (Form No. 1)

You can obtain Form No. 1 (the application for registering a partnership firm) through the official website of the Registrar of Firms (RoF) in your respective state. In this application form, you provide details such as the firm name, nature of business, main location, partner details, joining dates, and duration. All partners, or their authorized agents, must sign this application.

-

Submit Documents to the Registrar of Firms

Along with the application form, you generally submit the original notarized Partnership Deed, required registration fee (varies by state), a copy of the firm’s PAN card, address proof for the firm's business place (rent agreement/utility bill), PAN cards and address proofs for all partners, and an affidavit declaring all provided details are correct.

-

Receive Your Registration Certificate

After successful verification, the Registrar of Firms will issue a Certificate of Registration with a unique firm number. This Certificate is your legal proof for registration.

-

Open a Current Bank Account for the Firm

Once the firm's registration is complete and you have the Certificate of Registration and the firm's PAN card, you can open a current bank account in the partnership firm's name. You need this account to manage the firm's finances. Depending on turnover and business activity, the firm may also need GST registration.

Note: Different states in India may have varying procedures, forms, fees, and stamp duty for partnership firm registration, as allowed under the Indian Partnership Act, 1932. It's advisable to consult a legal expert to ensure accurate drafting of the partnership deed.

Partnership Firm Registration Timeline

The partnership firm registration process in India typically takes 10 to 15 working days from application submission to receiving the registration certificate, depending on state jurisdiction and document completeness.

- Document Preparation (2-3 Days): Drafting a partnership deed on stamp paper, collecting PAN cards, address proofs, photographs, and NOCs from all partners.

- Partnership Deed Execution (1-2 Days): Printing deed on appropriate stamp paper value as per state requirements, signing by all partners, and notarization.

- Application Submission (1 Day): Filing Form-1 (Application for Registration) with Registrar of Firms along with partnership deed and supporting documents.

- Document Verification (4-7 Days): ROF verifies submitted documents, partnership deed contents, and partner details for completeness and accuracy.

- Registration Certificate Issuance (1-2 Days): Upon approval, ROF issues Certificate of Registration with a unique registration number.

Fees of Partnership Firm Registration

The registration fees of a partnership firm is:

| Fee Category | Type | Cost/Range (INR) |

|---|---|---|

| Government Fees | Partnership deed stamp duty | varies by state and capital |

| Registration fees | 200 to 1,000 (varies by state) | |

| Name search and reservation | 400 to 800 | |

| Professional Fees | Partnership deed drafting | 5,000 to 8,000 |

| Legal consultation | 4,000 to 7,000 | |

| Registration assistance | 6,000 to 15,000 | |

| Post-Registration Costs | PAN card application | 110 (online) / 225 (physical) |

| TAN registration | Free online | |

| Bank account opening | Varies by bank | |

| GST registration (if applicable) | Free + Professional charges |

Advantages and Disadvantages of Partnership Firm Registration

Registering a partnership firm in India provides several key advantages:

- Legal Recognition & Protection: Formal legal standing enabling partners to sue third parties and enforce business contracts effectively. Registration provides legal proof of partnership existence and prevents ownership disputes.

- Enhanced Credibility & Trust: Demonstrates commitment to formal business practices and regulatory compliance, building customer confidence. Suppliers and vendors prefer registered entities for better payment security and reliability.

- Financial Advantages: Banks readily open current accounts and provide business loans with favorable terms to registered partnerships. Financial institutions offer higher credit limits and better interest rates to registered firms.

- Operational Benefits: Partnership deed terms help resolve internal disputes and clearly define partner roles. Registration facilitates branch expansion, franchise operations, and geographic growth.

- Tax Benefits: Partners claim legitimate business expense deductions, reducing overall tax liability. Registered firms qualify for MSME benefits, government subsidies, and incentive programs.

- Succession Planning: Formal partnership terms outline succession procedures and asset distribution methods. Registration simplifies partner entry, exit, and ownership transfer processes.

Disadvantages of Partnership Firm Registration

- Unlimited Personal Liability: Partners remain personally liable for all business debts without limitation. Personal assets can be seized to settle firm obligations.

- Joint and Several Liability: Each partner bears responsibility for actions and debts created by other partners. One partner's mistakes affect all partners financially.

- Limited Growth Potential: Cannot issue shares or raise capital through public equity offerings like companies. Funding options restricted to partner contributions and loans.

- Restricted Ownership Transfer: Partners cannot freely transfer ownership interests without unanimous consent from other partners. Exit strategies are more complex than corporate structures.

- No Separate Legal Entity: The firm does not exist independently from partners under Indian law. Cannot own property, sue, or be sued in its own name.

- Partnership Instability: Death, retirement, insolvency, or withdrawal of any partner can dissolve the entire partnership. Business continuity depends on all partners.

- Management Deadlocks: Equal partnership rights can lead to decision-making conflicts and operational delays. Disagreements may stall business operations.

Post Registration Compliance Requirements for a Partnership Firm

Post partnership firm registration, businesses must maintain ongoing tax, regulatory, and documentation compliance to ensure legal validity and operational continuity.

- Income Tax Return Filing: Partnership firms must file income tax returns annually using Form ITR-5. Filing deadlines are 31st July for non-audited firms and 31st October for audited firms. Tax audit becomes mandatory when turnover exceeds ₹1 crore for business or ₹50 lakh for professional services.

- Tax Deduction at Source (TDS) Compliance: When liable to deduct TDS, firms must deduct TDS, deposit amounts on time, file quarterly TDS returns (Forms 24Q, 26Q, 27Q), and issue Form 16/16A TDS certificates.

- GST Registration and Compliance: Registered firms must file monthly/quarterly GSTR-1 and GSTR-3B, submit annual GSTR-9, maintain compliant invoices, and generate e-way bills as required.

- Partnership Deed Amendment and Re-Registration: Any change in partnership structure requires drafting an amended deed on stamp paper and re-registration filing with the ROF using Form-3.

- Annual Return Filing (State-Specific): Some states require annual renewal applications or declarations filed with the ROF to maintain active status.

- Books of Accounts Maintenance: Firms must maintain proper accounting books including cash book, general ledger, P&L account, balance sheet, vouchers, and bank statements.

- Shops and Establishment Act Registration: Firms must obtain this registration from local municipal authorities and renew licenses as per state rules.

- Industry-Specific License Compliance: Depending on activities, firms may need FSSAI registration, professional tax registration, trade license, IEC registration, or pollution control clearances.

- PAN and TAN Updates: Maintain updated PAN for tax identification and TAN for TDS compliance.

- Form-A Submission (When Required): Some states require periodic Form-A submissions providing updated partner details and filing status.

Partnership Firm Registration Certificate and Status Check

This certificate is proof that your partnership firm exists in the eyes of the law. It gives your firm official legal recognition under the Indian Partnership Act. It authorizes the opening of a bank account in the firm’s name, legal status to enter into contracts, and conduct business transactions.

If you feel a partnership might not be the best fit for your business, you can also complete your company registration online to set up other types of business entities easily.

Need Help with Partnership Firm Registration?

Let our experts handle the legal drafting and registration process for you. Get started today!

Frequently Asked Questions (FAQs)

Is partnership firm registration mandatory in India?

No, partnership firm registration is not mandatory under the Indian Partnership Act, 1932. However, registration is highly recommended as unregistered firms cannot file lawsuits against third parties, enforce contracts in courts, or claim certain legal benefits.

What is the minimum and maximum number of partners allowed?

A partnership firm requires a minimum of 2 partners and can have a maximum of 50 partners. If partners exceed 50, the business must be registered as a company under the Companies Act, 2013.

How long does partnership firm registration take?

The registration process typically takes 7-15 working days from application submission to certificate issuance. The timeline may vary depending on document completeness and state-specific processing speeds.

What is the cost of registering a partnership firm?

Registration fees vary by state, typically ranging from ₹500 to ₹2,000 as government charges. Additional costs include stamp paper for partnership deed (₹200-₹1,000 depending on state), professional service fees (₹3,000-₹10,000), and notarization charges.

Can a partnership firm be registered online?

Yes, many states now offer online partnership firm registration through their respective Registrar of Firms portals. However, the partnership deed must still be executed on physical stamp paper and notarized before uploading.

What is a partnership deed and is it mandatory?

A partnership deed is a legal agreement defining partner rights, duties, profit-sharing ratio, capital contributions, and operational terms. While not legally mandatory, it is strongly recommended to prevent disputes and establish clear business terms.

Can foreign nationals become partners in an Indian partnership firm?

Yes, foreign nationals can become partners, but at least one partner must be an Indian resident. Foreign partners must have valid visa documentation and comply with FEMA (Foreign Exchange Management Act) regulations.

What documents are required for partnership firm registration?

Essential documents include partnership deed on stamp paper, PAN cards of all partners, identity proof (Aadhaar/Passport/Voter ID), address proof of partners and firm, passport-size photographs, business address proof (rent agreement/NOC/utility bills), and Form-1 application.

Is a PAN card mandatory for partnership firm registration?

Yes, obtaining a PAN card in the firm's name is mandatory before applying for registration with the Registrar of Firms. The PAN is required for taxation, banking operations, and GST registration.

Can a partnership firm own property?

No, a partnership firm does not have a separate legal entity status under the Indian Partnership Act, 1932. Property must be held in the names of individual partners, though it can be registered as partnership property in the partnership deed.

When is GST registration required for partnership firms?

GST registration is mandatory if the firm's annual turnover exceeds ₹40 lakhs for goods or ₹20 lakhs for services. Certain businesses like e-commerce operators, interstate suppliers, and specific service providers must register regardless of turnover.

Can an unregistered partnership be registered later?

Yes, an unregistered partnership can apply for registration at any time during its operation. Partners simply need to submit Form-1 with the partnership deed and required documents to the Registrar of Firms.

What happens if a partner dies or retires?

Unless the partnership deed states otherwise, the death, retirement, or insolvency of a partner dissolves the partnership firm. However, the deed can include provisions for continuation of business with remaining partners or admission of new partners.

Can the partnership deed be amended after registration?

Yes, the partnership deed can be amended with mutual consent of all partners. The amended deed must be executed on stamp paper, signed by all partners, and filed with the Registrar of Firms using Form-3 for updating registration records.

What is the difference between partnership firm and LLP?

Partnership firms have unlimited personal liability for partners and no separate legal entity status, while LLPs (Limited Liability Partnerships) offer limited liability protection and exist as separate legal entities under the LLP Act, 2008. LLPs have higher compliance requirements but better protection for partners' personal assets.