Formsy

Formsy

Cancellation of GST Registration for Business Closure

Get your business GST-registered with expert guidance. Access input tax credits, expand across India, and stay compliant with all government requirements.

- Form REG-16 & GSTR-10 Filing Services

- Input Tax Credit Reversal Support

- Avoid Penalties with Proper Compliance

- End-to-End GST Cancellation Management

- Trusted GST Cancellation Experts in India

Enter your details to receive a full quote and consultation

What is the Cancellation of GST Registration?

Cancellation of GST registration is the official process of terminating your Goods and Services Tax registration with the GST authorities, resulting in the cessation of your status as a registered taxpayer under the GST regime in India.

This usually happens when:

- You stop doing business

- Your business is transferred or merged

- You don’t need GST anymore (like your turnover is below the limit)

- You break the GST rules, and the government cancels it

Once your GST registration is cancelled, you are no longer required to collect GST from customers, pay GST to the government, claim input tax credit on purchases, or file monthly, quarterly, or annual GST returns.

Legal Framework for GST Cancellation

GST registration cancellation is governed by Section 29 of the Central Goods and Services Tax (CGST) Act, 2017, and Rules 20 to 22 of the CGST Rules. The cancellation process can be initiated either voluntarily by the registered taxpayer or compulsorily by the GST department through proper officers when specific non-compliance conditions are met.

GST Cancellation vs Surrender: Understanding the Difference

GST surrender is a voluntary, taxpayer-initiated process for closing registration, while GST cancellation can be either voluntary or compulsory by authorities for non-compliance. Both require filing final return GSTR-10 and settling all outstanding tax liabilities before completion.

| Basis | GST Cancellation | GST Surrender |

|---|---|---|

| Definition | Permanent termination of GST registration by authorities or taxpayer |

Voluntary discontinuation of GST registration by the registered taxpayer |

| Initiated By | GST officer (compulsory) or taxpayer (voluntary) |

Only by the registered taxpayer voluntarily |

| Reason | Non-compliance, non-filing of returns for 6 months, fraud, business closure |

Business closure, turnover below threshold, voluntary withdrawal |

| Process | Authorities issue show cause notice (Form GST REG-17); taxpayer responds via Form GST REG-18 |

Taxpayer directly files application in Form GST REG-16 on GST portal |

| Nature | Can be involuntary (compulsory by department) or voluntary |

Always voluntary and taxpayer-driven |

| Final Return | GSTR-10 must be filed within 3 months of cancellation order |

GSTR-10 must be filed within 3 months of surrender approval |

| Revocation | Can be revoked within 30 days using Form GST REG-21 |

Cannot be revoked once voluntarily surrendered |

| Legal Status | Permanent termination unless revoked | Permanent voluntary de-registration |

| Timeline | 15-30 days for processing after show cause notice response |

15-30 days for approval after application submission |

| Consequences | Cannot collect GST, file returns, or claim input tax credit |

Cannot collect GST, file returns, or claim input tax credit |

Who Can Apply for GST Registration Cancellation in India?

GST registration cancellation can be initiated by specific authorized entities as per Section 29 of the CGST Act, 2017, and CGST Rules 20-22. Understanding who has the legal authority to cancel GST registration is essential for ensuring compliance and avoiding penalties.

1. Registered Taxpayer (Voluntary Cancellation)

Who Qualifies:

- Any person or business holding an active GST registration certificate

- Registered taxpayers with valid GSTIN can voluntarily apply through GST portal

Eligibility Criteria:

- Business operations have permanently ceased or discontinued

- Annual turnover falls below the threshold limit (₹40 lakh for goods, ₹20 lakh for services)

- Business constitution changes requiring a new PAN (sole proprietorship converting to partnership or company)

- Business is transferred through sale, merger, amalgamation, de-merger, or leasing

- Registered person is no longer liable to pay GST under the law

- Voluntary registrants who fail to commence business within prescribed time

2. GST Proper Officer (Compulsory/Suo Moto Cancellation)

Who Qualifies:

- Authorized GST officers appointed by the tax department

- Proper officers acting on their own initiative or upon request

Grounds for Department-Initiated Cancellation:

- Taxpayers fail to file GST returns for six consecutive months or more

- Non-commencement of business operations within six months of voluntary registration

- Issuance of invoices without actual supply of goods or services

- Contravention of GST Act provisions or violation of compliance requirements

- Registration obtained through fraud, willful misstatement, or misrepresentation

- Business operating from non-existent or unverifiable address

- Non-compliance with invoicing regulations or statutory requirements

3. Legal Heirs (Death of Sole Proprietor)

Who Qualifies:

- Legal heirs or successors of the deceased taxpayer in case of sole proprietorship

- Family members or legal representatives authorized to act on behalf of deceased's business

Required Documentation:

- Death certificate of the proprietor

- Proof of legal heirship (succession certificate, will, or family settlement deed)

- Authorization documents establishing right to act on behalf of deceased's business

Who Cannot Apply for GST Cancellation

Certain categories of GST registrants are ineligible to apply for voluntary cancellation:

• Tax Deductors and Tax Collectors (TDS/TCS):

- Persons registered specifically as Tax Deductors at Source (TDS) under Section 51.

- Tax Collectors at Source (TCS) registered under Section 52 of CGST Act.

- Mandatory registration for statutory tax collection obligations prevents cancellation.

• UIN Holders:

- Entities holding Unique Identity Numbers (UIN)

- Foreign diplomatic missions, embassies, and international organizations

- UIN required for claiming tax refunds on purchases, making cancellation ineligible

• Voluntary Registrants (Within First Year):

- Businesses that obtained voluntary GST registration (below threshold turnover)

- Cannot apply for cancellation until one year has elapsed from registration date

- Exception: business closure or transfer allows immediate cancellation

Impact & Consequences of GST Registration Cancellation

GST registration cancellation permanently terminates your status as a registered taxpayer under the Goods and Services Tax regime, resulting in significant operational, financial, and compliance implications for your business.

Immediate Business Impact

- Loss of Tax Collection Authority: Once GST registration is cancelled, businesses cannot legally collect GST from customers or issue GST-compliant tax invoices. All invoices issued after cancellation must be without GST charges.

- Inability to Issue Tax Invoices: Cancelled taxpayers lose the authority to issue GST invoices, which directly affects B2B transactions where clients require proper tax invoices for input tax credit claims.

- Business Operations Restriction: Companies requiring mandatory GST registration cannot continue operations without valid registration, forcing business suspension until fresh registration is obtained.

- Customer Relationship Impact: B2B clients may discontinue business relationships since they cannot claim input tax credit on purchases from cancelled GST taxpayers.

Input Tax Credit Consequences

- Loss of ITC Claims: After cancellation, businesses cannot claim input tax credit on any purchases, increasing operational costs significantly.

- ITC Reversal on Closing Stock: Taxpayers must reverse input tax credit availed on closing stock and capital goods in the final return GSTR-10.

- Buyer's ITC Impact (Retrospective Cancellation): If registration is cancelled with retrospective effect, buyers who claimed ITC on purchases from the cancelled taxpayer may face ITC disallowance and tax demands.

Compliance & Return Filing Impact

- Suspension of Regular GST Returns: Taxpayers cannot file regular GSTR-1 and GSTR-3B returns after the cancellation date.

- Mandatory Final Return Filing : GSTR-10 (final return) must be filed within three months of cancellation order date, reporting all closing stock, outstanding liabilities, and ITC reversals.

- Outstanding Liability Remains: Cancellation does not absolve taxpayers from paying pending tax dues, interest, and penalties for periods before cancellation.

- Continued Scrutiny Risk: GST authorities can issue notices under Sections 73 and 74 for discrepancies in previously filed returns even after cancellation.

Financial & Tax Implications

- Payment of All Outstanding Dues: Businesses must clear all pending GST liabilities, including taxes, interest, late fees, and penalties before or during cancellation.

- Interest Accumulation: Outstanding tax liabilities continue to accrue interest until full payment is made, even after registration cancellation.

- No Refund of Unutilized Credit: Any remaining input tax credit in the electronic credit ledger cannot be claimed as refund and is forfeited upon cancellation.

- Loss of Composition Scheme Benefits: Composition taxpayers lose the simplified tax scheme and reduced compliance burden after cancellation.

Legal & Regulatory Consequences

- Liability for Pre-Cancellation Period: Taxpayers remain legally liable for all tax obligations, audits, and assessments for periods before cancellation date.

- Retrospective Cancellation Impact: Department-initiated cancellations can be effective retrospectively, creating serious tax liabilities and penalties for the entire non-compliance period.

- Supply Chain Disruption: Vendors and clients may face complications in reconciling transactions, claiming ITC, and maintaining compliant records.

- Penalties for Violations: If cancellation occurs due to fraud, wilful misstatement, or GST law violations, taxpayers may face additional penalties and prosecution.

Business Reputation & Credibility Impact

- Loss of GST Compliance Status: Cancelled registration damages business reputation with clients, vendors, banks, and investors who rely on GST compliance for credibility.

- Banking & Credit Challenges: Financial institutions may reject loan applications or reduce credit limits due to cancelled GST status, viewing it as a non-compliance indicator.

- Marketplace & Platform Restrictions: E-commerce platforms, government tenders, and B2B marketplaces require active GST registration, making cancelled businesses ineligible for participation.

When to Cancel GST Registration: Reasons & Eligibility Criteria

Learn about when you need to apply for cancellation and how much time you have to do it.

- Voluntary: You can apply for cancellation anytime after registration if you're no longer required to be under GST.

- By Officer: Cancellation starts automatically if you don't file returns for 6 months (or 3 months for composition).

- Important: Apply for cancellation within 30 days of stopping business or for any other reason.

Types of GST Cancellation: Voluntary vs Compulsory Cancellation

| Aspect | Voluntary Cancellation | Compulsory Cancellation (by Officer) |

|---|---|---|

| Initiated By | Registered taxpayer | GST officer/tax department |

| Nature | Proactive and self-initiated | Reactive due to non-compliance |

| Reason | Business closure, turnover below threshold, transfer, or no longer liable |

Non-filing of returns for 6 months, fraud, violations, non-compliance |

| Application Form | Taxpayer files Form GST REG-16 | Officer issues show cause notice Form GST REG-17 |

| Response Required | No response needed (taxpayer applies directly) | Taxpayer must respond within 7 days via Form GST REG-18 |

| Timeline | 30 days for approval after application | 7 days to respond + 30 days for cancellation order |

| Effective Date | From application date or business closure date | Can be retrospective from violation date |

| Revocation Allowed | No (voluntary surrender cannot be revoked) | Yes, within 30 days using Form GST REG-21 |

| Penalties | Generally no penalties if compliant | May attract penalties, interest, prosecution |

| Impact | Smooth and planned exit | Disruptive, affects business operations |

| Cancellation Order | Form GST REG-19 issued by officer | Form GST REG-19 after show cause proceedings |

| Final Return | GSTR-10 within 3 months | GSTR-10 within 3 months |

Documents Required for GST Registration Cancellation

Mandatory Documents:

- PAN card of business/proprietor

- GST registration certificate (GSTIN)

- Proof of business closure (board resolution, dissolution deed, or affidavit)

- Final GST return (GSTR-10) within 3 months

- Tax payment receipts for all cleared dues

- Closing stock details (inputs, semi-finished goods, finished goods)

- Capital goods details held in stock

- Outstanding liability details

- Last return filed details

- Bank account details

- Legal documents (partnership deed or incorporation certificate)

Supporting Documents (if applicable):

- Authorization letter

- Death certificate (for legal heir cancellation)

- Aadhaar card

- Address proof (electricity bill or rent agreement)

- Balance sheet and payment details

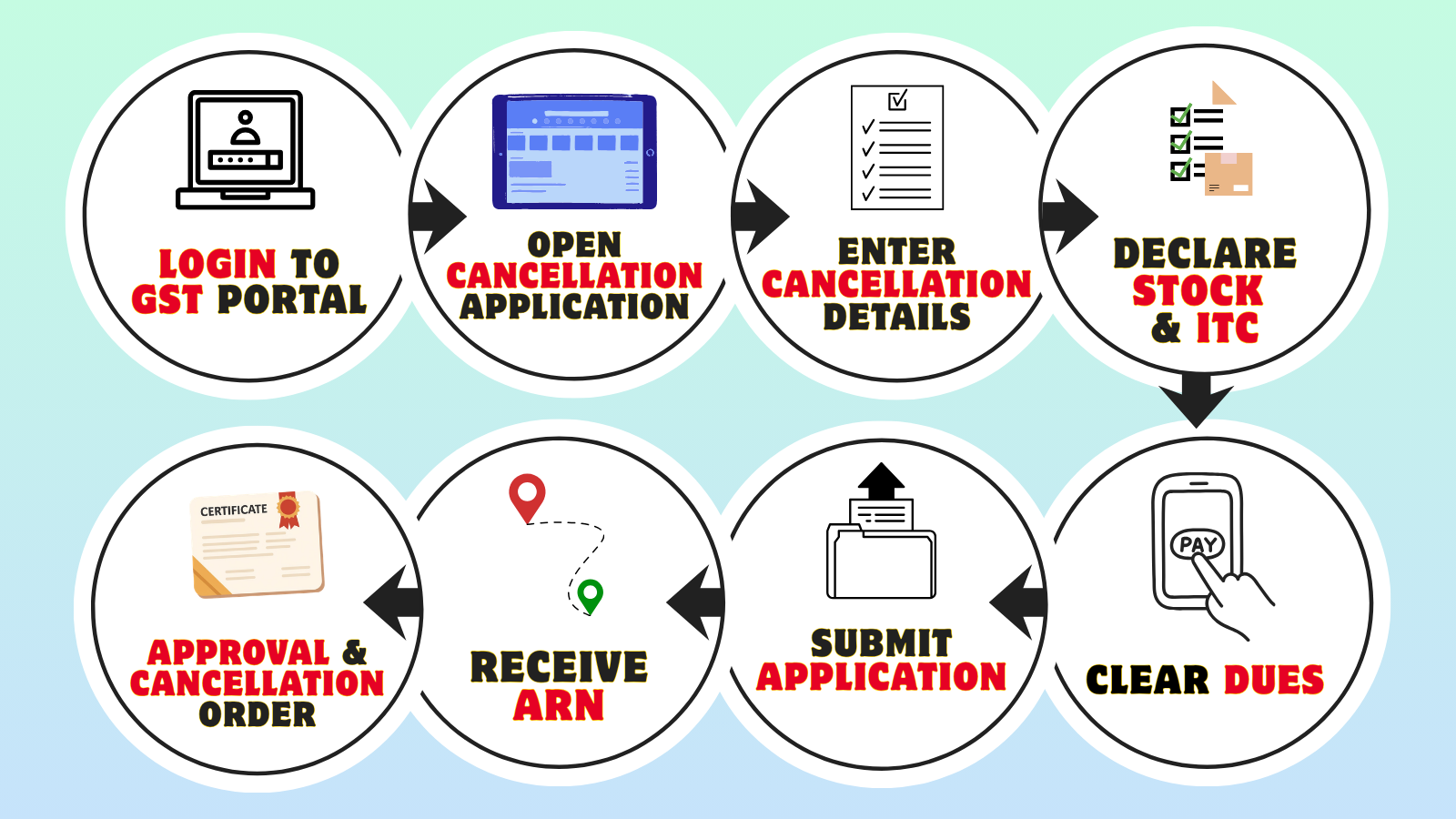

How to Cancel GST Registration Online: Step-by-Step Process

Follow these easy steps to apply for cancellation through the GST portal.

- Log in to gst.gov.in

- Go to Services > Registration > Application for Cancellation

- Enter Details like:

- Reason for cancellation

- Date of cancellation

- Details of remaining stock and ITC

- Pay Dues: Make sure all returns are filed and dues are cleared with the cancellation effective date.

- Submit Application using Digital Signature Certificate (DSC) or OTP (EVC).

- Get ARN: You’ll receive an Acknowledgement Reference Number to track your application.

- Officer Review: GST officer may ask for more info—reply if needed.

- Cancellation Order: If everything is okay, you’ll get Form GST REG-19 with the cancellation date.

GST Cancellation Timeline: Processing Time & Approval Duration

Voluntary Cancellation (Taxpayer-Initiated):

- Application submission via Form GST REG-16

- GST officer review and verification period: 30 working days from application date

- Cancellation order issued in Form GST REG-19 within 30 days

- Total processing time: 15-30 days (typically)

- May extend to 1 month depending on application complexity and officer workload

Compulsory Cancellation (Officer-Initiated):

- Show cause notice issued in Form GST REG-17

- Taxpayer response deadline: 7 working days via Form GST REG-18

- Officer review after response: 30 days for cancellation order

- Cancellation order in Form GST REG-19

- Total timeline: 37-40 days (7 days response + 30 days processing)

| Process | Timeline | Form |

|---|---|---|

| Voluntary cancellation application | 30 working days | GST REG-16 |

| Show cause notice response | 7 working days | GST REG-18 |

| Cancellation order issuance | 30 days from application/response | GST REG-19 |

| Final return filing | 3 months from cancellation | GSTR-10 |

| Revocation application | Within 30 days of cancellation | GST REG-21 |

| Revocation processing | 30 days | GST REG-22 |

GST Cancellation Fees & Charges: Complete Cost Breakdown

Cancelling your GST registration on the GST portal does not involve any government charges. However, if you take help from a tax consultant or a CA, they may charge a professional fee based on the service provided.

Common Mistakes to Avoid During GST Cancellation

- Failing to file GSTR-10 within 3 months of cancellation leads to penalties and notices.

- Applying without paying all pending taxes, interest, late fees, and penalties.

- Not reversing ITC on closing stock and capital goods invites tax demand notices.

- Submitting wrong GSTIN, business details, or closing stock data causes rejection.

- Assuming cancellation is immediate and stopping compliance before official approval.

- Choosing wrong effective date creates compliance mismatches.

Need Help with GST Cancellation?

Let our experts handle the GST cancellation process for you. Get started today!

Frequently Asked Questions (FAQs)

What is GST registration cancellation?

GST registration cancellation is the process of formally terminating your GST registration with the tax authorities when you no longer conduct taxable business, cease operations, or fall below the threshold turnover limit. Cancellation can be voluntary (taxpayer-initiated) or compulsory (department-initiated).

When should I cancel my GST registration?

You should cancel GST registration when your business has permanently ceased taxable supplies, annual turnover falls below the threshold limit (₹40 lakh for goods, ₹20 lakh for services), you've changed business constitution (sole proprietorship to partnership), the business has been transferred or merged, or operations have been discontinued.

What is the difference between voluntary and compulsory GST cancellation?

Voluntary cancellation occurs when a taxpayer applies for cancellation using Form GST REG-16 due to business closure or falling below turnover thresholds. Compulsory cancellation happens when GST officers cancel registration due to non-filing of returns for six consecutive months, non-payment of taxes, or GST law violations.

What is Form GST REG-16?

Form GST REG-16 is the application form used to apply for cancellation of GST registration through the GST portal. It requires details about the reason for cancellation, closing stock, outstanding liabilities, and supporting documents.

How do I cancel GST registration online?

Log in to www.gst.gov.in, navigate to Services > Registration > Application for Cancellation of Registration, fill Form GST REG-16 with reason for cancellation and closing stock details, upload supporting documents, verify using DSC or EVC, and submit to receive an Application Reference Number (ARN).

What documents are required for GST cancellation?

Required documents include PAN card, proof of business closure (board resolution, dissolution deed, or affidavit), final GST return (GSTR-10), tax payment receipts clearing all dues, and authorization letter if using a consultant.

How long does GST cancellation take?

The GST officer processes the cancellation application within 30 working days from submission, provided all documents are correct and there are no outstanding dues. You'll receive a cancellation order in Form GST REG-19.

What is GSTR-10 and when should I file it?

GSTR-10 is the final return that must be filed within three months of the cancellation order date. It reports closing stock, details of taxable supplies made after cancellation, and any outstanding tax liabilities.

Can I continue business operations after applying for GST cancellation?

Until your GST registration is officially cancelled by the GST officer, you must continue complying with all GST obligations including filing returns, issuing tax invoices, and paying taxes.

What happens to input tax credit (ITC) after GST cancellation?

Unused input tax credit cannot be claimed or carried forward after GST cancellation. You must reverse any ITC availed on closing stock and capital goods as per GST rules in GSTR-10.

Can I revoke GST cancellation after it's approved?

Yes, you can apply for revocation of GST cancellation within 30 days of the cancellation order using Form GST REG-21. The GST officer will review your application and may restore registration by issuing Form GST REG-22.

What are the consequences of GST cancellation?

After cancellation, you cannot make taxable supplies or collect GST from customers, must pay all outstanding tax liabilities with interest and penalties, lose eligibility to claim input tax credit, and cannot issue tax invoices.

Can GST registration be cancelled for non-filing of returns?

Yes, GST officers can initiate compulsory cancellation if you fail to file GST returns for six consecutive months or more. You'll receive a show cause notice before cancellation.

Do I need to pay pending taxes before cancellation?

Yes, all pending GST liabilities, including taxes, interest, and penalties must be cleared before applying for cancellation. Upload tax payment receipts as supporting documents with your application.

What is the cancellation effective date?

The cancellation effective date depends on the reason: for voluntary cancellation, it's the date mentioned in your application or when you ceased business operations; for compulsory cancellation, it's determined by the GST officer based on non-compliance dates. The effective date is mentioned in the cancellation order Form GST REG-19.