Formsy

Formsy

GST Registration Online in India

Get your business GST-registered with expert guidance. Access input tax credits, expand across India, and stay compliant with all government requirements.

- GST Registration Support for Tax Compliance

- Unlock input tax credits and reduce your tax liability

- Expand your business legally across all Indian states

- Post-Registration Compliance and Advisory Services

Enter your details to receive a full quote and consultation

What is GST Registration?

Under Goods And Services Tax (GST), businesses whose turnover exceeds the threshold limit of Rs.40 lakh or Rs.20 lakh or Rs.10 lakh as the case may be, must register as a normal taxable person. For a few types of small businesses/professionals as defined under the CGST Section 10 of Composition scheme, this threshold turnover limit is Rs.1.5 crore/Rs.50 lakh respectively. For certain businesses, registering its business under the GST law is mandatory despite turnover it makes. The process of obtaining registration or GSTIN (GST Identification Number) in all these cases is known as GST registration. If the entity carries on business without registering under GST when mandated, it is an offence under GST and heavy penalties will apply. GST registration usually takes between 12-15 working days. Team Formsy can help you obtain GST registration services faster in 3 easy steps!

Benefits of GST Registration

Here are some advantages of registering for GST:

Legal Tax Collection & Enhanced Credibility

- Authorized GST Collection Rights: Registered businesses gain legal authority to collect GST from customers, ensuring transparent tax collection aligned with government regulations. This official approval minimizes compliance errors and establishes your business as a legitimate tax-collecting entity.

- Build Trust Through GST Invoicing: Issue GST-compliant invoices to clients and vendors, instantly boosting your business credibility in the market. This is especially useful for formal entities such as sole proprietorships, partnership firms, LLPs, and private limited companies. Your registered GSTIN demonstrates authenticity and reliability, strengthening stakeholder confidence in your operations.

Input Tax Credit Benefits

- Lower Your Tax Liability: Claim input tax credit on GST paid for business purchases, significantly reducing your overall tax burden and improving cash flow. This credit mechanism helps optimize working capital and enhances financial efficiency.

- Maintain Accurate Financial Records: GST credit claims encourage systematic record-keeping and proper accounting practices, ensuring smooth audits and seamless vendor relationships. Well-maintained documentation prevents compliance issues and simplifies tax filing processes. Good records also support smoother GST return filing and audit preparation.

- Seamless Regulatory Compliance: Integrate input tax credit claims with statutory requirements for hassle-free adherence to GST regulations. This alignment simplifies tax calculations and ensures your business meets all legal obligations.

Expanded Business Growth Opportunities

- Access Government Tenders & B2B Contracts: GST registration unlocks eligibility for government procurement projects and large B2B contracts, creating valuable growth opportunities. This qualification opens doors to high-value partnerships and strategic business collaborations. Businesses also strengthen eligibility through proper income tax compliance and, where applicable, MSME registration.

- Enable Interstate & Online Business Operations: Expand your market reach beyond geographical boundaries with unrestricted interstate commerce and e-commerce capabilities. Your GST registration facilitates nationwide business expansion and enhances brand visibility across India.

Full Legal Compliance Protection

- Avoid Penalties & Legal Issues: Stay compliant with Indian tax laws and protect your business from GST-related penalties, notices, and legal complications. Proper registration ensures you operate within the legal framework without regulatory risks.

- Simplify Tax Audits & Filing: Regular GST returns linked to your GSTIN streamline audit processes and strengthen your business's legal standing. Organized compliance records make tax assessments straightforward and hassle-free.

- Strengthen Market Reputation: Demonstrate reliable financial practices through accurate GST compliance, building strong stakeholder confidence and enhancing your competitive position in the market.

Pan-India Business Expansion

- Seamless Interstate Operations: Eliminate state-wise tax barriers and operate smoothly across all Indian states with unified GST compliance. This single registration framework simplifies logistics and ensures efficient goods movement nationwide.

- E-commerce Platform Integration: Sell nationwide through major online marketplaces like Amazon, Flipkart, and others with your GST registration. This enables digital expansion, increases sales potential, and maximizes your brand's online presence. Many growing businesses formalize further through private limited company registration or LLP registration.

Types of GST Registration in India

Businesses must comprehend the various forms of GST registration in order to guarantee correct compliance and optimize tax advantages.

• Normal Taxpayer Registration

Normal Taxpayer registration is the most common GST category for regular businesses exceeding prescribed turnover thresholds. This registration allows businesses to collect GST legally, claim Input Tax Credit (ITC) on purchases, and issue tax invoices to customers. Businesses registered as normal taxpayers have no expiry date and must file monthly, quarterly, and annual returns based on their turnover. This category provides full benefits of the GST system including seamless interstate trade and participation in government tenders.

• Composition Scheme Registration

The Composition Scheme offers simplified compliance for small businesses, allowing them to pay GST at significantly reduced rates without the burden of monthly filings. Eligible businesses file only quarterly returns, reducing administrative workload considerably. However, composition taxpayers cannot claim input tax credit, must issue only bills of supply (not tax invoices), and cannot make inter-state supplies or sell through e-commerce platforms.

• Casual Taxable Person Registration

Casual Taxable Person registration suits businesses conducting temporary or seasonal operations in locations where they have no fixed establishment. This category is ideal for traders attending exhibitions, seasonal vendors, or businesses testing new markets temporarily. Registration requires advance tax payment based on estimated turnover, remains valid for 90 days, and can be extended by another 90 days.

• Non-Resident Taxable Person Registration

Foreign entities supplying goods or services in India without establishing a permanent business address must obtain Non-Resident Taxable Person registration. Similar to casual registration, it requires advance tax deposits and has limited validity periods, typically 90 days extendable based on business requirements. This ensures international businesses operating temporarily in India remain tax compliant.

• Non-Resident Online Services Distributor (OIDAR)

Foreign businesses providing Online Information Database Access or Retrieval services like streaming platforms, software subscriptions, cloud services, and digital content to Indian customers must register under this specialized category. Registration is mandatory regardless of turnover, requires advance tax payments, and involves specific reporting requirements for cross-border digital services taxation.

• Input Service Distributor (ISD) Registration

From April 1, 2025, Input Service Distributor registration became mandatory for businesses with multiple branches or units under the same PAN needing to distribute input tax credit on centrally received services. The registered office or headquarters acts as the ISD, proportionately distributing GST credit paid on shared services like IT support, legal consultancy, or marketing to various branches based on their turnover. This ensures efficient credit utilization across geographically dispersed business locations. Businesses with multiple branches may also need additional place of business in GST updates where applicable.

• Special Economic Zone (SEZ) Developer/Unit Registration

Businesses operating within Special Economic Zones must register as SEZ Developers or SEZ Units to access significant tax benefits and export incentives. SEZ units are treated as foreign territory for trade operations, making supplies to and from SEZs equivalent to exports and imports. These entities enjoy zero-rated supplies without upfront tax payment, can claim full input tax credit refunds, and benefit from customs duty exemptions. Businesses involved in cross-border trade may also require import export code registration.

• Tax Deductor at Source (TDS) / Tax Collector at Source (TCS) Registration

Government departments, public sector undertakings, and notified entities deducting or collecting GST at source must obtain TDS/TCS registration regardless of their supply activities. TDS applies when government entities make payments to suppliers (typically 2% deduction), while TCS applies to e-commerce operators collecting tax from seller transactions on their platforms. These registrants must deposit collected amounts monthly and file quarterly returns.

• E-commerce Operator Registration

E-commerce platforms facilitating supply of goods or services must register under GST irrespective of turnover. They're responsible for collecting Tax at Source (TCS) at 1% of net taxable supplies made through their platform. From November 2025, the GST 2.0 framework introduces simplified automated registration for e-commerce operators, with automatic approval within three working days for qualifying applicants. Operators must file monthly and annual returns, deposit TCS with the government, and ensure all sellers maintain valid GST registration.

GST Registration Thresholds & Key Features

| Registration Type | Turnover Threshold | Tax Rate/Special Feature | Validity Period | ITC Benefit |

|---|---|---|---|---|

| Normal Taxpayer (Regular States - Goods) |

₹40 lakhs | Standard GST rates | No expiry | Yes |

| Normal Taxpayer (Regular States - Services) |

₹20 lakhs | Standard GST rates | No expiry | Yes |

| Normal Taxpayer (Special Category States) |

₹20 lakhs | Standard GST rates | No expiry | Yes |

| Normal Taxpayer (Northeastern States) |

₹10 lakhs | Standard GST rates | No expiry | Yes |

| Composition Scheme | Up to ₹1.5 crore | 1% (Traders), 5% (Manufacturers), 6% (Services) |

No expiry | No |

| Composition Scheme (Special Category States) |

Up to ₹75 lakhs | 1% (Traders), 5% (Manufacturers), 6% (Services) |

No expiry | No |

| Casual Taxable Person | No threshold | Standard GST rates | 90 days (extendable to 180 days) |

Yes |

| Non-Resident Taxable Person | No threshold | Standard GST rates | 90 days (extendable) | Yes |

| OIDAR Services | No threshold | Standard GST rates | Limited validity | Yes |

| Input Service Distributor | No threshold | Credit distribution only | No expiry | N/A |

| SEZ Developer/Unit | No threshold | Zero-rated supplies | No expiry | Yes |

| TDS/TCS Registration | No threshold | 2% (TDS), 1% (TCS) | No expiry | N/A |

| E-commerce Operator | No threshold | 1% TCS collection | No expiry | Yes |

India has different GST registration threshold limits for Special Category States compared to regular states.

Special Category States receive lower thresholds to promote economic development and reduce compliance burden on small businesses in regions with challenging terrain, lower income levels, and infrastructural difficulties. These states also receive higher central funding and various tax benefits to boost industrialization and employment.

| State Category | States/UTs | Goods Threshold | Services Threshold |

|---|---|---|---|

| Regular States (Opted for ₹40L) |

Gujarat, Maharashtra, Karnataka, Tamil Nadu, Delhi, Bihar, Punjab, Haryana, Rajasthan, UP, MP, Kerala, Goa, West Bengal, Odisha, Chhattisgarh, Jharkhand, Chandigarh, etc. |

₹40 lakhs | ₹20 lakhs |

| Regular State (Status Quo) |

Telangana | ₹20 lakhs | ₹20 lakhs |

| Special Category (Opted for ₹40L) |

Jammu & Kashmir, Ladakh, Assam, Himachal Pradesh | ₹40 lakhs | ₹20 lakhs |

| Special Category (₹20L Threshold) |

Arunachal Pradesh, Meghalaya, Sikkim, Uttarakhand, Puducherry |

₹20 lakhs | ₹20 lakhs |

| Special Category (₹10L Threshold) |

Manipur, Mizoram, Nagaland, Tripura | ₹10 lakhs | ₹10 lakhs |

Components of GST: CGST, SGST, IGST, and UTGST

• CGST (Central Goods and Services Tax)

CGST is levied by the Central Government on intra-state supplies of goods and services, governed by the Central Goods and Services Tax Act, 2017. This tax applies when both the supplier and buyer are located within the same state or Union Territory. Revenue collected from CGST is deposited directly with the Central Government. Businesses can claim Input Tax Credit (ITC) on CGST paid, which can be set off against CGST liability first, and any remaining credit can then be used to pay IGST liability.

• SGST (State Goods and Services Tax)

SGST is imposed by State Governments on the same intra-state transactions where CGST applies, ensuring states receive their share of tax revenue. Both CGST and SGST are levied concurrently on every intra-state supply, with each component typically constituting 50% of the total GST rate. Revenue from SGST goes directly to the respective state government, replacing previous state-level taxes like VAT, purchase tax, luxury tax, and octroi. SGST rates are uniform across states but vary by product or service category.

• IGST (Integrated Goods and Services Tax)

IGST applies to inter-state transactions when goods or services are supplied between different states or Union Territories. It is also levied on all imports into India and exports from India, with exports being zero-rated. IGST is collected entirely by the Central Government and equals the combined rate of CGST and SGST (100% of the GST rate). The Central Government later shares the SGST portion with the destination state where goods or services are consumed. This mechanism ensures seamless tax flow across state borders and eliminates tax cascading in interstate commerce. Businesses involved in import-export operations may also require IEC registration and, in customs-linked cases, ICEGATE registration.

• UTGST (Union Territory Goods and Services Tax)

UTGST replaces SGST in Union Territories without legislative assemblies, applying to intra-territory transactions within these regions. Currently, UTGST is applicable in Union Territories including Chandigarh, Andaman & Nicobar Islands, Lakshadweep, Dadra & Nagar Haveli and Daman & Diu. The structure and rates remain the same as SGST, with UTGST collected by Union Territory administrations for transactions occurring within their jurisdictions. Like SGST, UTGST is levied alongside CGST at equal rates for intra-territory supplies.

How GST Components Work Together?

| Transaction Type | Location Example | GST Components Applied | Tax Split | Revenue Distribution | Example Calculation (18% GST on ₹1,000) |

|---|---|---|---|---|---|

| Intra-State (Within Same State) | Seller in Gujarat → Buyer in Gujarat | CGST + SGST | Equal split (9% + 9%) | 50% to Central Govt, 50% to State Govt | CGST: ₹90, SGST: ₹90, Total: ₹180 |

| Intra-UT (Within Union Territory) | Seller in Chandigarh → Buyer in Chandigarh | CGST + UTGST | Equal split (9% + 9%) | 50% to Central Govt, 50% to UT Administration | CGST: ₹90, UTGST: ₹90, Total: ₹180 |

| Inter-State (Between Different States) | Seller in Maharashtra → Buyer in Karnataka | IGST Only | Single tax (18%) | Collected by Centre, SGST portion shared with destination state | IGST: ₹180, Total: ₹180 |

| Inter-State (State to UT) | Seller in Delhi → Buyer in Lakshadweep | IGST Only | Single tax (18%) | Collected by Centre, UTGST portion shared with destination UT | IGST: ₹180, Total: ₹180 |

| Imports into India | Foreign supplier → Indian buyer | IGST + Customs Duty | Full GST rate as IGST | Collected by Central Govt at customs | IGST: ₹180 + applicable customs duty |

| Exports from India | Indian supplier → Foreign buyer | Zero-rated (0% IGST) | No tax charged | Refund of input taxes available | No GST charged, ITC refund claimable |

Eligibility for GST Registration

GST registration is mandatory for businesses meeting specific criteria and advisable for others seeking tax benefits and market credibility.

• Turnover-Based Registration

Businesses must register for GST when aggregate turnover exceeds ₹40 lakhs for goods suppliers and ₹20 lakhs for service providers in regular states. Special category states have a ₹20 lakh threshold, while northeastern states require registration at ₹10 lakhs for both goods and services. Aggregate turnover includes all taxable supplies, exempt supplies, exports, and inter-state supplies under the same PAN.

• Compulsory Registration Categories

Certain business categories require GST registration regardless of turnover:

- Interstate suppliers conducting business across state borders

- E-commerce operators and sellers using platforms like Amazon, Flipkart, Swiggy

- Casual taxable persons operating temporarily in different locations

- Non-resident taxable persons supplying goods or services in India

- Businesses liable under reverse charge mechanism

- Input service distributors with multiple branches (mandatory from April 1, 2025). Related branch updates may also involve additional place of business in GST.

- Agents of suppliers facilitating transactions

- OIDAR service providers offering digital services from abroad to Indian customers

- Tax deductors and collectors including government departments

• Voluntary GST Registration Benefits

Small businesses below threshold limits can opt for voluntary GST registration online to claim Input Tax Credit (ITC), reduce tax liability, and build business credibility. Voluntary registration enables issuing GST invoices, accessing B2B contracts, participating in government tenders, and expanding into interstate trade. This is particularly useful for newly formed entities such as sole proprietorships, partnership firms, and LLPs.

Documents Required for GST Registration in India

Regardless of the specific business type, the following documents are mandatory for GST registration:

- PAN Card: Mandatory for all businesses as GSTIN is linked to the business’s PAN.

- Aadhaar Card: Required for verification in speeding up the process through Aadhaar authentication.

- Proof of Business Address: Needed to verify the main business location (owned, rented, or shared).

- Proof of Business Constitution: Needed to verify the business identity. This may include documents from partnership firm registration, LLP registration, OPC registration, or private limited company registration.

- Bank Account Details: Required to link GST with your business’s bank account.

- Passport-size Photos: Needed for identification of proprietors or authorized signatories.

- Digital Signature Certificate (DSC): Mandatory for companies and LLPs for online submission.

- Authorization Letter/Board Resolution: Gives authority to a person to handle GST matters for the business.

Note: The required documents can vary based on your business structure (e.g., a Partnership Firm requires a Partnership Deed, while an LLP needs its LLP Agreement). For a personalized checklist tailored to your business, consulting a professional is recommended.

Guide to Online GST Registration Process

The entire GST registration process is digital, free of government fees, and can now be completed with automatic approval within three working days for qualifying applicants under the GST 2.0 framework.

-

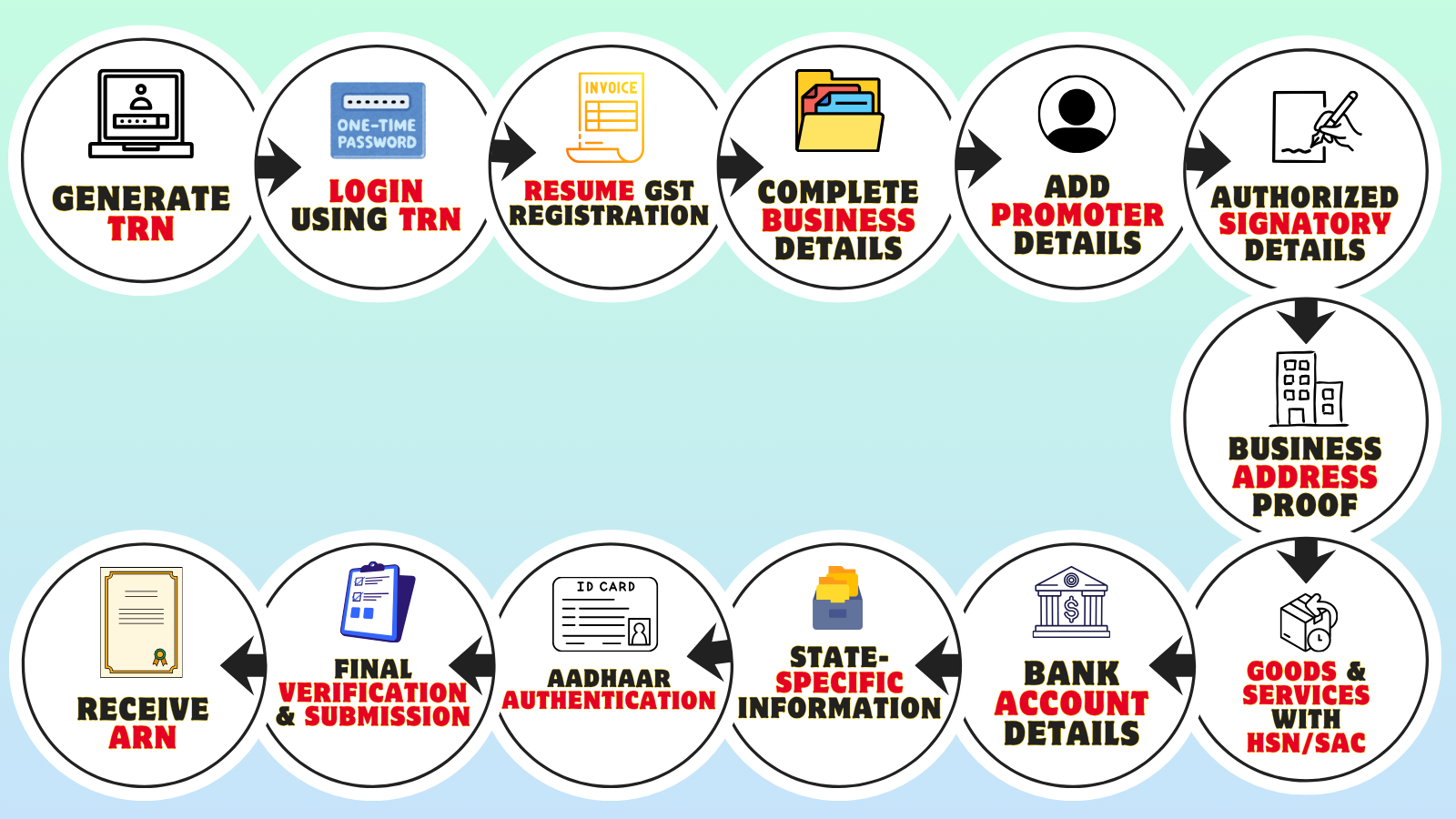

Step 1: Generate Temporary Reference Number (TRN)

- Access the GST Portal: Visit the official GST website at www.gst.gov.in to begin your GST registration online process. Navigate to the homepage and click on "Services" > "Registration" > "New Registration" to initiate your application.

- Complete Part A of Form GST REG-01: Select "Taxpayer" as the registration category, choose your State and District from the dropdown menu, and enter your business legal name and Permanent Account Number (PAN). Provide a valid mobile number and email address for OTP verification purposes.

- OTP Verification for GST Registration: Separate One-Time Passwords (OTPs) will be sent to your registered mobile number and email address for verification. Enter both OTPs in the designated fields to authenticate your contact details. Upon successful verification, the system generates a unique 15-digit Temporary Reference Number (TRN) displayed on your screen.

-

Step 2: Login Using TRN

Return to the GST portal homepage and select "Services" > "Registration" > "New Registration" > "Temporary Reference Number (TRN)". Enter your generated TRN along with the captcha code and click "Proceed" to receive fresh OTPs on your registered email and mobile.

-

Step 3: Access Your Saved GST Application

After logging in with TRN authentication, click on "My Saved Applications" to view your draft application. Select the edit option to continue completing Part B of Form GST REG-01 with detailed business information.

-

Step 4: Enter Business Details for GST Registration

Fill in your trade name (different from legal name), business constitution type, district, and select your business codes including commissionerate code, division code, and range code. Enter the date of business commencement and the date from which GST liability arises. Choose "Yes" or "No" to opt for the Composition Scheme if your business qualifies under the turnover threshold of ₹1.5 crore.

-

Step 5: Add Promoter and Partner Information

Provide comprehensive details of all promoters, partners, or directors including their full name, PAN, Aadhaar number, date of birth, gender, contact information, and Director Identification Number (DIN) if applicable. Upload recent photographs in PDF or JPEG format (under 1MB) for each stakeholder.

-

Step 6: Designate Authorized Signatory for GST Compliance

Specify the authorized signatory who will handle GST compliance and filing on behalf of your business. Provide their complete details including name, designation, PAN, Aadhaar authentication, contact information, and upload supporting identity documents.

-

Step 7: Submit Business Address Proof

Enter your principal place of business with complete address details including building name, street, locality, and PIN code. Upload address proof documents such as electricity bill, property tax receipt, rent agreement with NOC, or municipal khata copy. Indicate the nature of premises ownership (owned, rented, leased, or shared) and add details of any additional business locations or branch offices. Where valid, this may also be supported by a virtual office address arrangement.

-

Step 8: Declare Goods and Services with HSN/SAC Codes

List up to five primary goods with their corresponding Harmonized System of Nomenclature (HSN) codes and up to five main services with their Service Accounting Codes (SAC). Select the most relevant products and services representing your core business activities for accurate GST classification.

-

Step 9: Provide Bank Account Details

Submit your business bank account number, IFSC code, bank name, and branch address. Upload a cancelled cheque leaf or bank statement as proof of account ownership (Note: Bank details became non-mandatory at registration since December 27, 2018, and can be provided later during return filing).

-

Step 10: Add State-Specific Information

Enter additional state-specific details if required by your jurisdiction, such as Professional Tax (PT) employee code, State Excise License number, Shops and Establishment registration number, or other local registrations.

-

Step 11: Complete Aadhaar Authentication for Fast Processing

Choose Aadhaar-based authentication for expedited processing and automatic approval within three working days under the new GST 2.0 framework. Alternatively, skip Aadhaar authentication to undergo manual verification, which may take longer for approval. From February 2025, biometric authentication became mandatory for certain applicant categories.

-

Step 12: Final Verification and Submission

Review all entered information thoroughly for accuracy before final submission. Tick the declaration checkbox confirming the authenticity of provided information. Authenticate and submit your GST registration application using one of three methods:

- Digital Signature Certificate (DSC) - Mandatory for companies, LLPs, and foreign entities

- e-Sign using Aadhaar OTP - Available for proprietorships, individuals, and partnerships

- Electronic Verification Code (EVC) - OTP sent to registered mobile number

-

Receive Application Reference Number (ARN)

Upon successful submission of your GST registration online application, the system generates a unique 15-digit Application Reference Number (ARN) sent to your registered email address and mobile number via SMS. Use this ARN to track your GST registration status on the portal under "Services" > "Registration" > "Track Application Status".

GST Registration Timeline and Validity

The time taken for the GST registration process varies based on several factors:

- With Aadhaar Authentication: Usually approved within 3–7 working days. If no action is taken by the officer in 7 days, it's auto-approved.

- Without Aadhaar Authentication: The process may take 21–30 days or more due to possible physical verification or additional document checks.

Factors Affecting GST Registration Timeline:

- Incomplete or Incorrect Info: Mistakes or missing details cause delays.

- Document Checks: Authorities verify all documents carefully.

- Business Type: Some entities may take longer (e.g., Casual Taxable Persons, DSC users).

- Government Load: High volumes can slow down processing.

- Delayed Response to Queries: Taking too long to respond to clarification requests from the GST officer can extend the timeline.

Validity of GST Registration

The validity of a GST registration certificate varies depending on the type of taxpayer:

- Regular Taxpayers: GST registration is permanent unless cancelled or surrendered; no renewal needed if compliance is maintained.

- Casual Taxable Persons: Registration is temporary and valid for 90 days, which is extendable by another 90 days.

- Non-Resident Taxable Persons: Registration is valid for the period mentioned in the certificate or as per the GST payment duration, whichever is shorter.

GST Registration Fees and Penalties

The registration fees may vary depending on different scenarios:

- Most Regular Businesses: There is no government fee for GST registration. No additional requirements apply.

- Casual Taxable Persons: While registration itself is free, applicants must submit a security deposit ranging from ₹500 to ₹10,000, depending on the nature of the business and state-specific rules.

- Non-Resident Taxable Persons: Registration is also free, but a mandatory security deposit between ₹500 and ₹10,000 is required. This applies to temporary or foreign business entities operating in India.

So, if a business crosses the GST threshold and fails to register, it can face heavy penalties along with interest on unpaid tax. In some cases, businesses that stop taxable operations may later require cancellation of GST registration.

- General Penalty: ₹10,000 or 10% of the tax due — whichever is higher.

- In Case of Fraud/Deliberate Evasion: ₹10,000 or 100% of the tax due — whichever is higher.

Post-Registration: GST Compliance and Return Filing

GST Return Filing

- File GSTR-1 monthly (by 11th) or quarterly (by 13th) to report all sales and outward supplies

- Submit GSTR-3B monthly (by 20th) or quarterly (by 22nd/24th) with tax liability summary and ITC claims

- Reconcile purchases with auto-generated GSTR-2B before claiming input tax credit

- File GSTR-9 annual return by December 31st for businesses above ₹2 crore turnover

E-Invoicing Compliance

- Generate e-invoices for B2B transactions if turnover exceeds ₹1 crore from April 2025

- Report invoices to Invoice Registration Portal (IRP) within 30 days for IRN generation

- Include IRN and QR code on all invoice copies for authenticity verification

E-Way Bill Management

- Generate e-way bills before transporting goods worth over ₹50,000

- Ensure base documents are not older than 180 days from January 2025

- Use mandatory two-factor authentication for e-way bill generation

Input Tax Credit Management

- Claim ITC only on purchases reflected in GSTR-2B after supplier filing and payment

- Reconcile ITC claims monthly with GSTR-2A/2B to identify discrepancies

- Avoid claiming ITC on blocked items under Section 17(5) like personal vehicles

GST Portal Security

- Enable Multi-Factor Authentication (MFA) mandatory from April 2025 for portal access

- Use OTP, email verification, or biometric authentication for enhanced security

Invoice and Documentation

- Issue GST-compliant invoices with GSTIN, HSN/SAC codes, and mandatory fields daily

- Maintain sequential numbering for all debit notes and credit notes

- Keep accurate records of all sales, purchases, and expenses with GST

Reverse Charge Mechanism

- Pay GST directly to government for specified services from unregistered suppliers

- Report RCM supplies separately in GSTR-3B by 20th of following month

Export Compliance

- File Letter of Undertaking (LUT) annually to export goods/services without paying IGST. Exporters usually also require import export code registration and may need ICEGATE registration.

- Renew LUT before March 31st each year for zero-rated exports

GST Audit Requirements

- Get accounts audited by CA/CMA if turnover exceeds ₹5 crore annually

- File GSTR-9C reconciliation statement along with GSTR-9 annual return

Compliance Monitoring

- Reconcile Tables 12 and 13 for outward supplies and ITC matching

- Respond promptly to automated notices for mismatches from GST authorities

- Maintain Books of Accounts with accurate stock details and transaction records

Penalty Avoidance

- Pay late filing penalty of ₹100 per day (₹50 CGST + ₹50 SGST) for delayed GSTR-3B

- Avoid 18% annual interest on unpaid tax liability by timely payment

- Prevent GSTIN cancellation by filing timely returns within consecutive periods

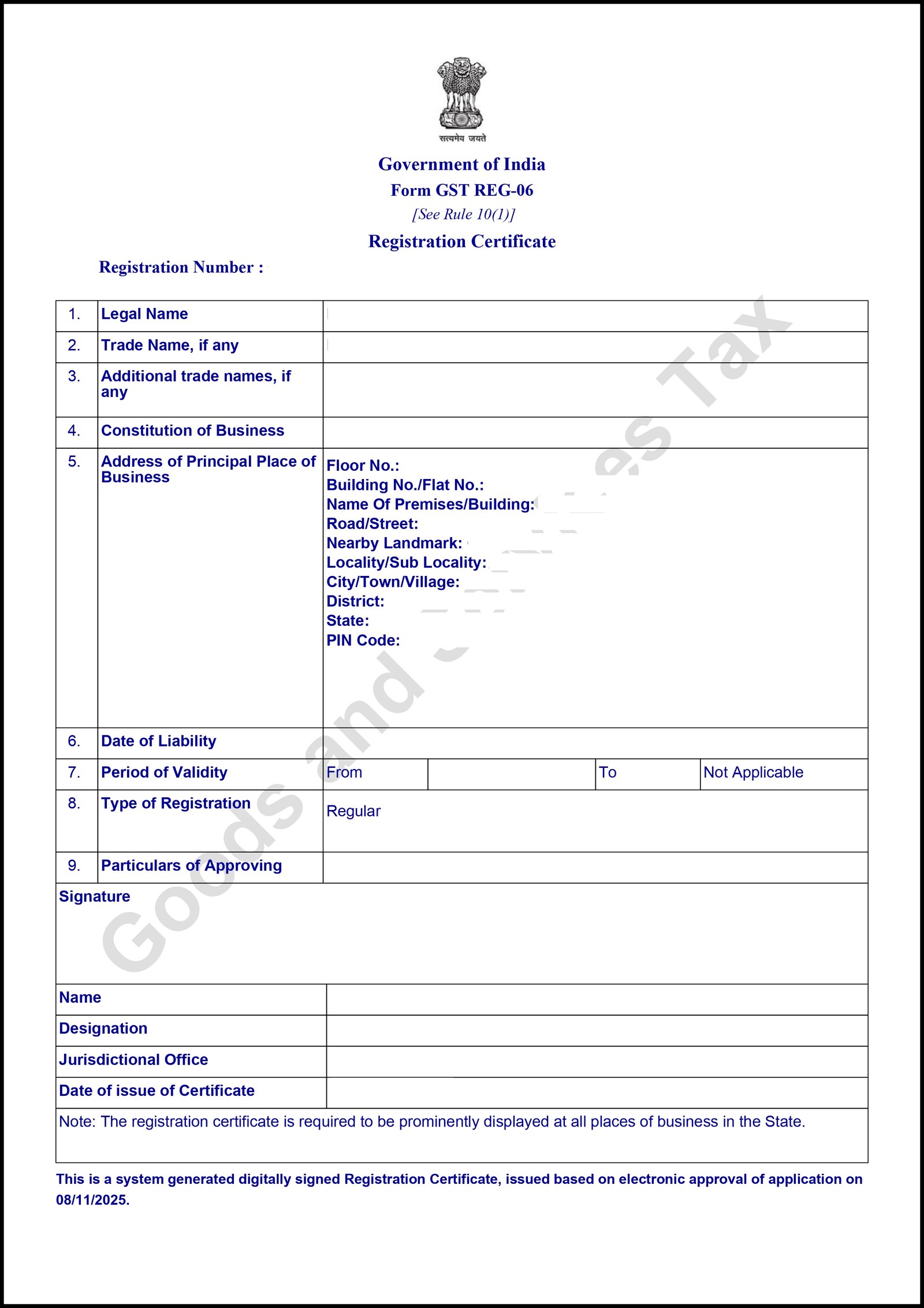

GST Registration Certificate

A GST Registration Certificate is an official document issued by the GST Department upon successful registration of a business under the GST system in India. It serves as legal proof that your business is recognized and registered to collect and remit GST. This also strengthens credibility for formal entities such as sole proprietorships, partnership firms, and private limited companies.

Key Details Included Under the GST Registration Certificate:

- GSTIN (Goods and Services Tax Identification Number)

- Legal Name and Trade Name of the Business

- Constitution of Business (Proprietorship, Partnership, etc.)

- Business Address

- Date of Registration

- Type of Registration (Regular, Composition, Casual, etc.)

How to Download Your GST Registration Certificate (Form GST REG-06)

Upon successful approval of your GST registration application, the GST authorities issue a certificate of registration in Form GST REG-06.

The physical copy is not provided by the authorities; it can only be downloaded from the GST Portal. To download your GST Registration Certificate:

- Log in to the GST Portal: Visit gst.gov.in and log in using your valid credentials (username and password).

- Navigate to Certificates: After logging in, click on "Services" > "User Services" > "View/Download Certificates".

- Download: The screen will display all certificates issued by the GST authorities. Locate "Registration Certificate (Form GST REG-06)" and click the "Download" icon under the "Download" column.

- Open and Print: The certificate will be downloaded in PDF format. You can then save it to your device or print a physical copy for your records.

Need Help with GST Registration?

Let our experts handle the entire GST registration process for you. Get started today!

Frequently Asked Questions (FAQs)

What is the GST registration turnover limit?

₹40 lakhs for goods suppliers and ₹20 lakhs for service providers in regular states. Special category states have ₹20 lakhs, while northeastern states require registration at ₹10 lakhs.

How long does GST registration take?

From November 1, 2025, low-risk applicants receive automatic approval within 3 working days under the GST 2.0 framework. Nearly 96% of applications qualify for this fast-track route.

Is GST registration free?

Yes, there are no government fees for GST registration on the official portal (www.gst.gov.in).

Can I register for GST voluntarily?

Yes, businesses below the threshold can voluntarily register to claim input tax credit, issue GST invoices, and build business credibility.

What documents are needed for GST registration?

PAN card, Aadhaar card, business address proof, bank account details with cancelled cheque, photographs of promoters, and digital signature certificate for companies/LLPs.

Is Aadhaar mandatory for GST registration?

From February 2025, Aadhaar authentication with biometric verification became mandatory for certain applicant categories. It enables faster automated approval.

When should I apply after crossing the threshold?

You must apply for GST registration within 30 days from the date you become liable (when turnover exceeds threshold limits).

Who must register regardless of turnover?

Interstate suppliers, e-commerce operators, casual taxable persons, non-resident taxable persons, reverse charge mechanism applicants, and OIDAR service providers.

What is TRN and ARN?

TRN (Temporary Reference Number) is generated after Part A submission for logging in. ARN (Application Reference Number) is issued after final submission to track application status.

Can I have multiple GST registrations?

Yes, you need separate GST registration for each state where you have a business location, as GSTIN is state-specific.

What happens after GST approval?

You receive a 15-digit GSTIN with GST Registration Certificate, enabling you to collect GST, claim input tax credit, and issue GST-compliant invoices.

Can I cancel my GST registration?

Yes, file Form GST REG-16 on the portal if you close business, fall below threshold (voluntary registration), or no longer conduct taxable activities.